In December of 2017, Congress passed, and President Trump signed, the Tax Cuts and Jobs Act of 2017 (the “Act”), ushering in lower tax rates, new tax provisions, and changes to popular deductions. These changes will, undoubtedly, impact the middle-market for merger and acquisition (M&A) transactions. The following provides a summary of the provisions likely having the biggest impact on M&A transactions.

Lower Rates

Tax rates were slashed across the board, with the corporate tax rate moving from graduated rates topping out at 35% to a flat, 21% corporate tax rate. The corporate Alternative Minimum Tax (AMT) was also eliminated, thereby leveling the playing field for some sectors that continuously paid the AMT.

In addition, flow-through businesses will see their tax rates drop through a combination of lower tax rates at the individual level and a new flow-through deduction equal to 20% of qualified business income for eligible taxpayers. The flow-through deduction begins to phaseout for some service-based businesses once the owner’s income exceeds $315,000.

Immediate Expensing

The Act bolsters two popular deductions that allow for accelerated depreciation - §179 and bonus depreciation. The §179 deduction limit was increased to $1,000,000 and indexed for inflation. In addition, the Act increased the phase-out threshold to begin at $2,500,000 of eligible assets placed in service.

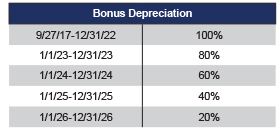

The Act also increased the bonus depreciation percentage to 100%, retro-actively, for property placed in service after September 27, 2017 through December 31, 2022. Beginning in 2023, the bonus depreciation percentage is phased down as follows:

- 80 percent for property placed in service during calendar year 2023;

- 60 percent for property placed in service during calendar year 2024;

- 40 percent for property placed in service during calendar year 2025; and

- 20 percent for property placed in service during calendar year 2026;

Interestingly, the Act modifies the definition of qualified property to include used property that was not used by the taxpayer before being acquired by the taxpayer. That is, otherwise eligible used assets may now qualify for bonus depreciation.

As a result, buyers have even more incentive to structure deals as an asset purchase, as any part of the purchase price allocable to bonus depreciable assets may be written off in the year the assets are placed in service.

Interest Expense Limitation

The Act limits the ability for some larger taxpayers to deduct their interest expense when paid or incurred. For companies with average annual gross receipts of more than $25 million of the prior three tax years, the ability to deduct its interest expense may be limited in tax years beginning after December 31, 2017. The $25 million limit is applied on an aggregate basis to any controlled group of corporations.

The Act limits the deduction for net interest expense (defined as interest expense, less interest income) incurred by a taxpayer to 30% of the company’s adjusted taxable income. For the first four years this provision is in effect (tax years 2018 through 2021), adjusted taxable income is determined without regard to depreciation or amortization. For tax years 2022 and thereafter, adjusted taxable income will take depreciation and amortization deductions into account.

This new limitation will certainly impact larger taxpayers’ financing mechanisms. Buyers that have historically financed new acquisitions via some debt may modify their financing approach in light of the new limitations on interest expense.

Tax Incentives

Popular tax incentives, such as the R&D tax credit and the Work Opportunity Tax Credit, were spared in the tax overhaul. In fact, with the lower corporate tax rate, the R&D tax credit became more valuable.

Overall Impact

Overall, the new tax bill is likely to be favorable to the M&A market, as buyers are likely to recoup their after-tax investment quicker.

About the Author

Michael J. Devereux II, CPA, CMP, is a partner and director of Manufacturing, Distribution & Plastics Industry Services for Mueller Prost. Devereux’s primary focus is on tax incentives and succession planning for the manufacturing sector. He regularly speaks at manufacturing conferences around the country on tax issues facing the manufacturing sector.