A recent report by the McKinsey Global Institute made several forecasts that, if correct, contain some bad news for ordinary investors and some very good news for owners of mid-size ($10MM to $100MM) companies.

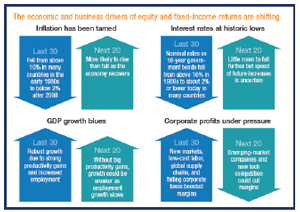

The Bad News For Investors: The return on equities over the next 20 years is expected to fall from an average of 6.5% (over the past 100 years) to four to five percent.

The Good News For Business Owners: Lower-than-historical returns will push corporate and private equity investors into the M&A marketplace looking for growth and better returns. More buyers competing for good businesses will push sale prices higher. The question is: Is your business one that buyers will compete to buy?

McKinsey's Findings

McKinsey predicts that, over the next 20 years, performance for equities will be between four and five percent and fixed investments (bonds) will be flat (0 to one percent.). It is hard to argue with McKinsey's reasons: slower rates of growth in GDP (especially China's), an end to falling inflation and interest rates, saturation in global marketplaces, slower gains in productivity, competition from emerging-market companies and the ever-present threat of disruptive new technologies.

In this cooler climate, corporations will be hard pressed to generate the organic growth necessary to satisfy investors clamoring for better returns. Instead, corporate buyers will look to "buy" growth by acquiring companies that will add to their top and bottom lines, and compete with their private equity counterparts to acquire the best companies.

|

The Power of Dry Powder

Dry powder is industry jargon for the money private equity funds have collected but not yet invested, and according to best estimates, there's a huge amount of it. Fund managers are competing to purchase companies that will generate the returns that their investors have come to expect.

The Implications For Investors—Both Public and Private

Barring any huge market adjustments (think Greece 2010, or Lehman Brothers collapse 2008), we expect investors (both public and private) to look for and invest in better-performing, alternative vehicles. With funds lowering their fees and investment minimums, smaller investors are joining their wealthier counterparts in dedicating part of their portfolios to private equity.

Is Your Company "The One?"

What kind of companies will these buyers pay top dollar for? Companies with solid histories of growth, management teams that have produced growth in the past and have the potential to continue to do so, diverse and loyal customer bases and presence in growing industries. If a target company can also cause create pain or gain for a buyer, the door opens to an outrageous price.

If you are interested in learning whether your company has what it takes to sell for an outrageous price, give us a call. We wrote the book on it. |