The numbers are in for 2018 and once again, M&A activity continued at a fever pitch. Analysts agree that 2018 was a seller’s market and buyers paid “multiples for smaller companies that we’ve never seen before.”

Congratulations to the sellers we represented during 2018 who took full advantage of this great market. But if you didn’t jump into the market in 2018, here’s a quick overview of what market experts think you can expect if you are thinking of selling your company in 2019.1

Opportunities for Sellers in 2019

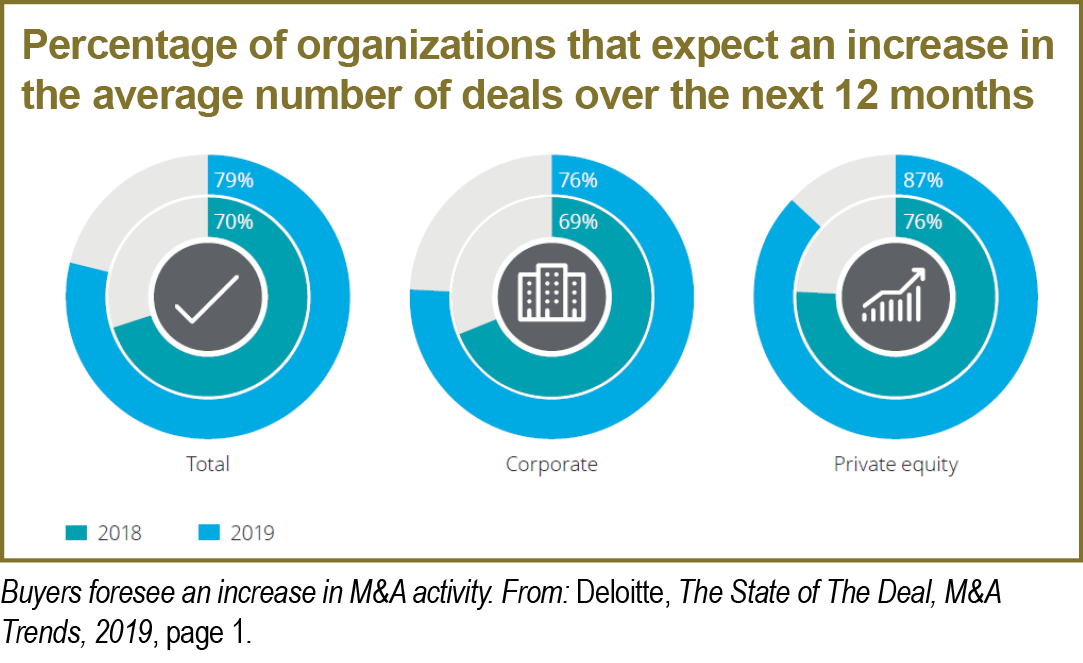

- Acquirers Are Hungry To Buy. Buyer appetite for quality acquisitions remains strong: “76% of M&A executives at US-headquartered corporations and 87% of M&A leaders at domestic private equity firms expect the number of deals their organizations will close over the next year to increase.”2

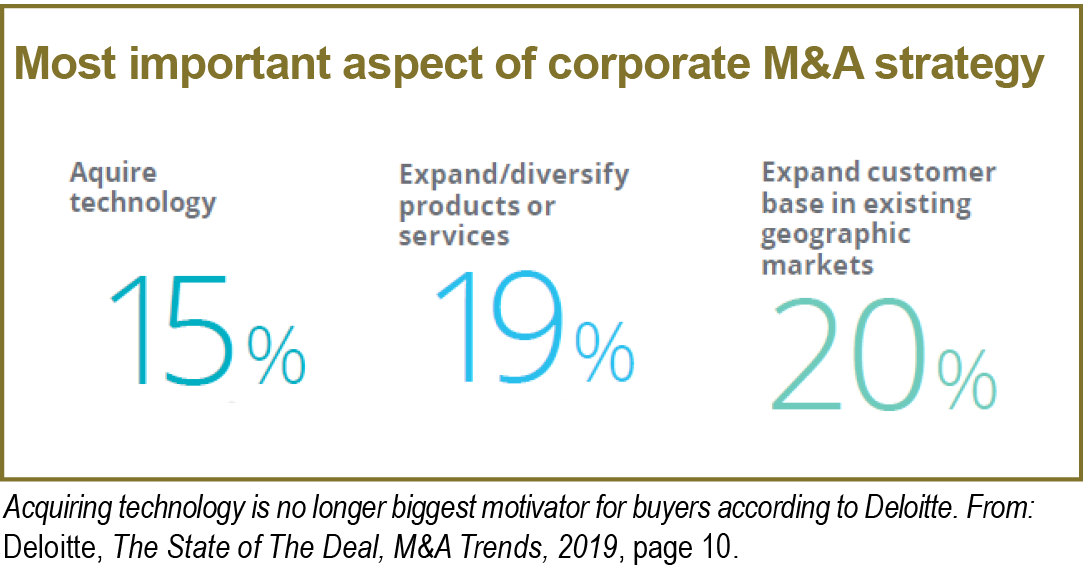

- Buyers Want More Than Technology. Along with acquiring technology, top motivators for buyers include expanding a customer base in an established geographic market and expanding or diversifying product and service lists.

- Buyers Expect To Compete. Buyers are well aware they must bring their best offers to the table to compete. “When trying to close a deal, you have to bring your ‘A’ game and be aggressive,” notes Richard B. Prestegaard, a partner in private equity firm that focuses on the middle market.3

Unknowns for Sellers in 2019

Both sellers and buyers are concerned with political and global economic uncertainty, but there are two issues for prospective sellers to consider.

- Quality Matters. Buyers will pursue only well-prepared companies at reasonable values. Buyers report that half of their deals fail to “generate the value they expected at the outset of a transaction,” for several reasons—including inaccurate valuations and a failure to achieve revenue synergies.4

- Sellers Must Be Prepared Before They Enter The Marketplace. Not only must a company be prepared for buyer scrutiny and packaged to attract attention, sellers must be realistic about their expectations. “Sellers are expecting sales off their most recent years, which has been their best year in five years,” notes one private equity group manager.5

At Clayton Capital Partners, we are experts in aligning a company’s best features with a buyer’s needs to secure a premium price. We look forward to another record year helping owners and stakeholders orchestrate transactions that maximize the value of their companies.

Kevin Short is the author of Sell Your Business For An Outrageous Price and the Managing Partner and CEO of Clayton Capital Partners, a St. Louis-based investment banking firm specializing in the sale and purchase of mid-size companies.

-

Johnson, Jeffrey W., Managing Director of Blackford Capital, as quoted in The M&A Advisor Symposium Report, Sector Trends and Outlook for 2019: Where We Go From Here, January, 2019, page 1.

-

Deloitte, The State of The Deal, M&A Trends, 2019, page 1.

-

Prestegaard, Richard B., High Road Capital Partners, as quoted in The M&A Advisor Symposium Report, Sector Trends and Outlook for 2019, page 4.

-

Ibid., Deloitte, pages 12-13.

-

Fine, Harvey, Managing Partner, Maris Global Capital, M&A Advisor Symposium Report, Sector Trends and Outlook for 2019, page 1.

|

|